Table of Content

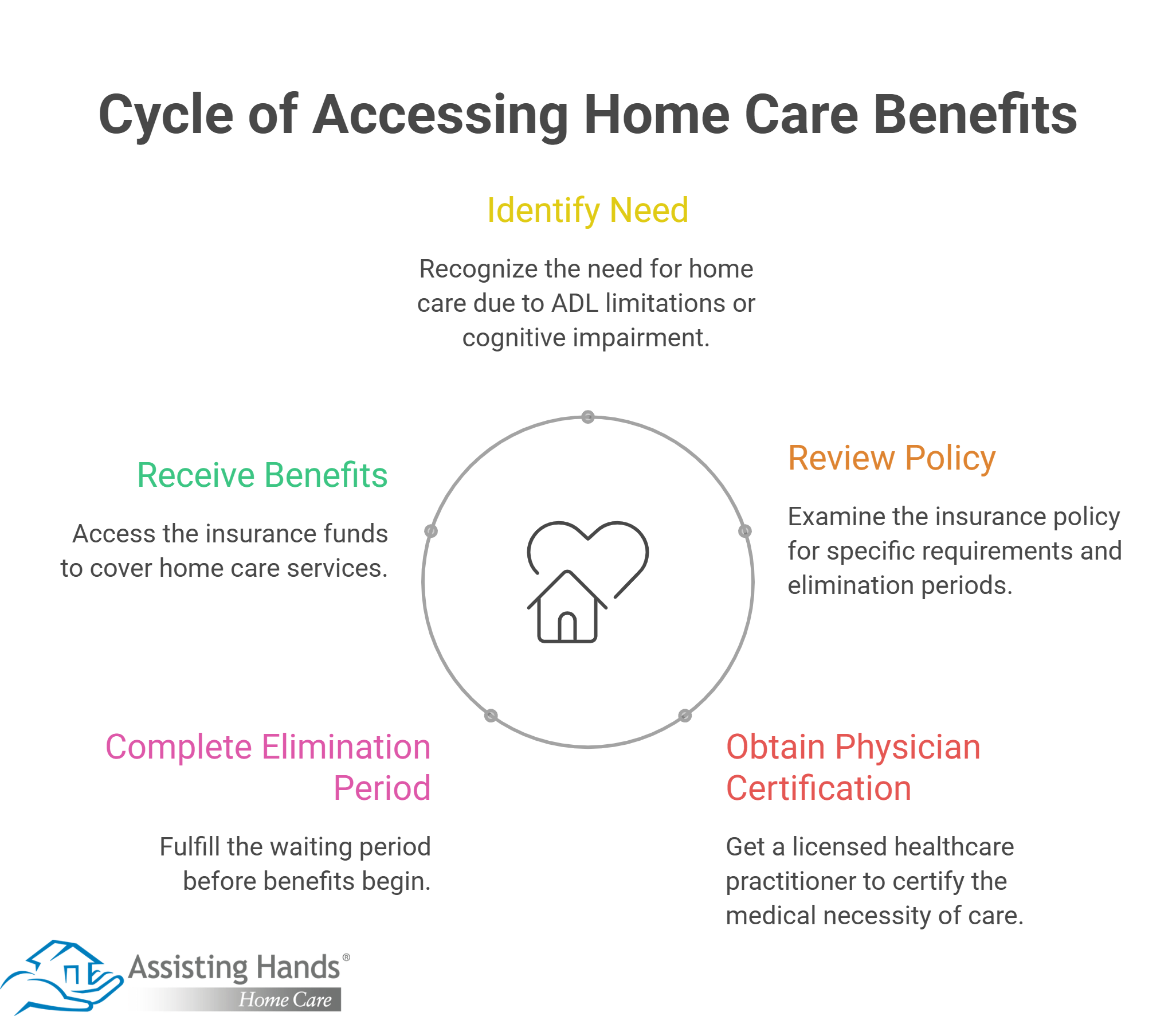

Long-term care insurance benefits for home care are typically triggered when a policyholder becomes unable to perform a certain number of activities of daily living (ADLs) or develops a severe cognitive impairment. Understanding these specific requirements helps families access necessary funds exactly when their senior loved ones need them most. Reviewing your specific policy details early on ensures a much smoother and faster claims process.

What Are Activities of Daily Living?

Activities of daily living, commonly referred to as ADLs, are the fundamental routine tasks individuals must manage to live safely and independently. Most long-term care insurance policies require a policyholder to need physical assistance or standby support with at least two out of six standard ADLs to trigger benefits. These standard ADLs typically include:

- Bathing

- Dressing

- Eating

- Transferring (moving to or from a bed or chair)

- Toileting

- Continence

Some seniors only require help with a few daily tasks so they can maintain their independence. However, those living with serious illnesses may need more extensive assistance. Luckily, you can rely on the exceptional professional Westminster 24-hour home care provided by Assisting Hands Home Care. Home can be a safer and more comfortable place to live with the help of an expertly trained and dedicated around-the-clock caregiver.

How Does Cognitive Impairment Trigger Coverage?

A severe cognitive impairment, such as Alzheimer’s disease or another advanced form of dementia, can independently trigger home care benefits even if the person can physically perform all ADLs. The insurance company generally requires a licensed physician’s diagnosis confirming the policyholder needs substantial constant supervision to protect his or her health and safety.

Aging in place can present a few challenges for seniors living with dementia. However, with professional dementia home care that offers Westminster families peace of mind, they can still live independently at home. Families can rely on Assisting Hands Home Care to provide their elderly loved ones with mental and social stimulation, timely medication reminders, assistance with meal prep, and much more. Our caregivers are available around the clock to help your loved one live a happier and healthier life.

What Is an Elimination Period?

An elimination period is essentially a deductible measured in time rather than dollars, acting as a waiting period before your insurance policy actually begins paying for home care services. During this timeframe, the policyholder is responsible for covering the costs of any required care out of pocket. These periods vary significantly by policy but most commonly range from 30 to 90 days.

Who Needs to Certify the Claim for Home Care?

To officially initiate your benefits, a licensed healthcare practitioner must certify the requested home care is medically necessary due to your physical or cognitive limitations. This usually involves a doctor, registered nurse, or licensed social worker submitting a detailed Plan of Care that outlines the specific home care services required to keep you safe.

Many seniors prefer aging in place over moving to assisted living facilities. If you or a senior loved one needs assistance to remain safe and comfortable while living at home, reach out to Assisting Hands Home Care, a leading Westminster home care agency. Our dedicated in-home caregivers can assist with meal prep, bathing and grooming, exercise, medication reminders, and many other important tasks. To learn about our high-quality in-home care options, give us a call today.

Frequently Asked Questions

Are family members paid to provide home care?

+

Most traditional long-term care insurance policies require you to use licensed home care agencies, meaning informal family caregivers cannot receive payment. However, certain policies offer a cash indemnity benefit that allows you to spend the funds however you choose, including paying relatives for their help.

Do all policies cover in-home care?

+

Not all policies automatically cover home care, as some older or strictly defined plans only pay for registered nursing home facilities. You must review your specific policy documents to confirm in-home assistance is an included benefit.

How long do home care benefits last?

+

The duration of your benefits depends entirely on the specific limits set when you purchased your policy, which might range from two years to an unlimited lifetime period. Once you exhaust the maximum benefit pool outlined in your contract, the insurance company will stop paying for care

Can a policy be cancelled after I file a claim?

+

Insurance companies cannot cancel a guaranteed renewable long-term care policy simply because your health declines or you file a valid claim. As long as you paid your required premiums continuously before the claim was triggered, your coverage will remain legally active.